Quant Letter: April 2025, Week-2

Weekly (86th Edition)

ArXiv

Finance

Enhanced Deep Hedging: A new deep hedging framework for index option portfolios, which includes surface-informed decisions and transaction costs, has been proposed and outperforms traditional methods in both simulated and historical data from 1996 to 2020. (2025-04-08, shares: 20)

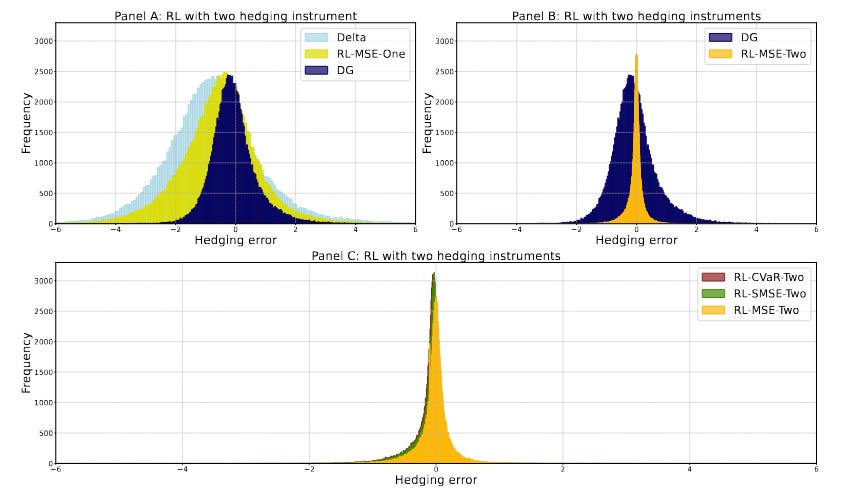

DRL Algorithms for Option Hedging: A comparison of eight Deep …