Quant Letter: August 2025, Week-4

105th Edition

ArXiv

Finance

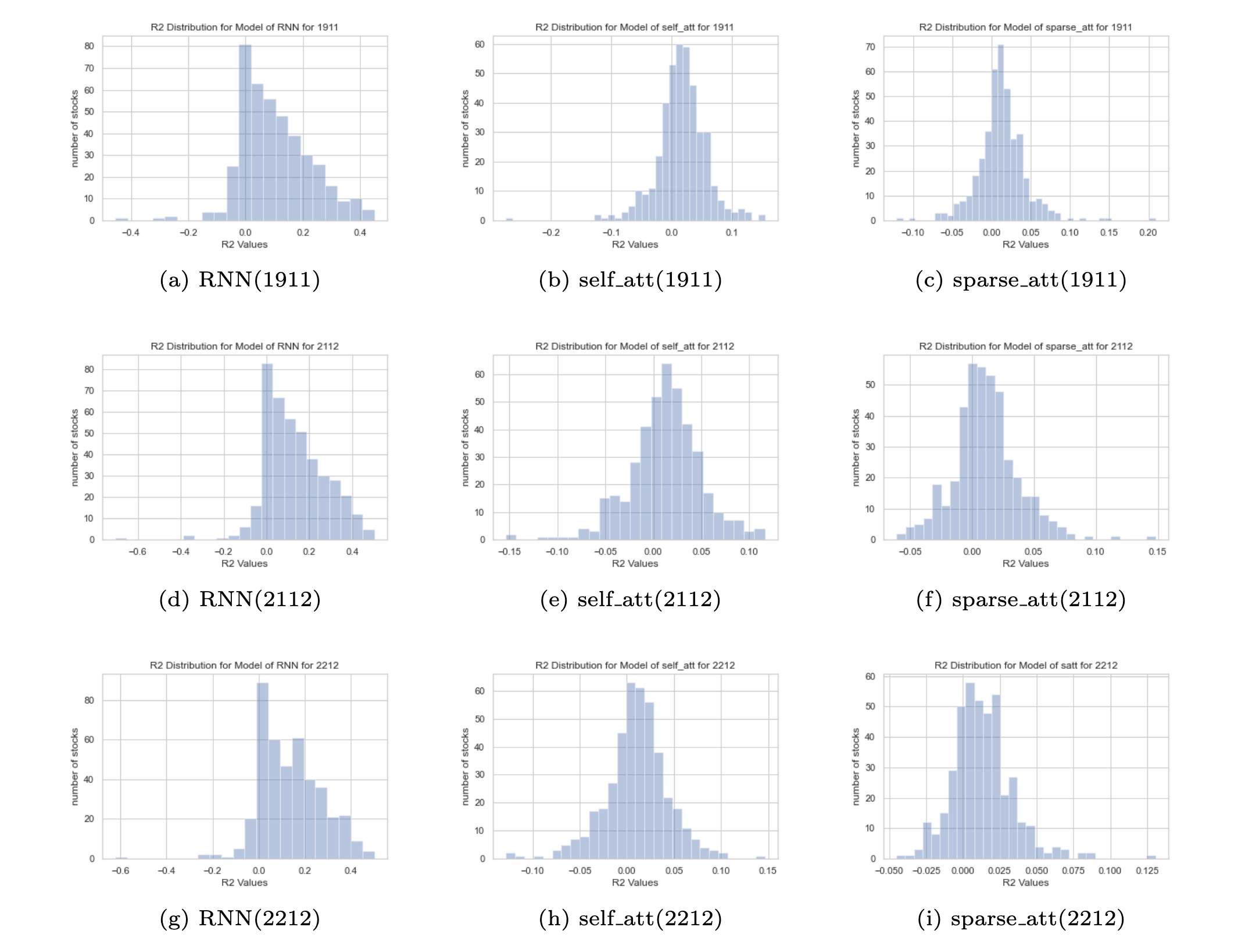

Asset Pricing with Attention Models: The study finds that pretrained RNN attention models can effectively derive returns and hedge risks in asset pricing, even during extreme market conditions like the COVID-19 pandemic. (2025-08-26, shares: 16)

ESG Risk Variables Algorithm: The research introduces a Hierarchical Variable Selection algorithm …