Quant Letter: July 2024, Week-3

Weekly (54th Edition)

SSRN

Recently Published

Quantitative

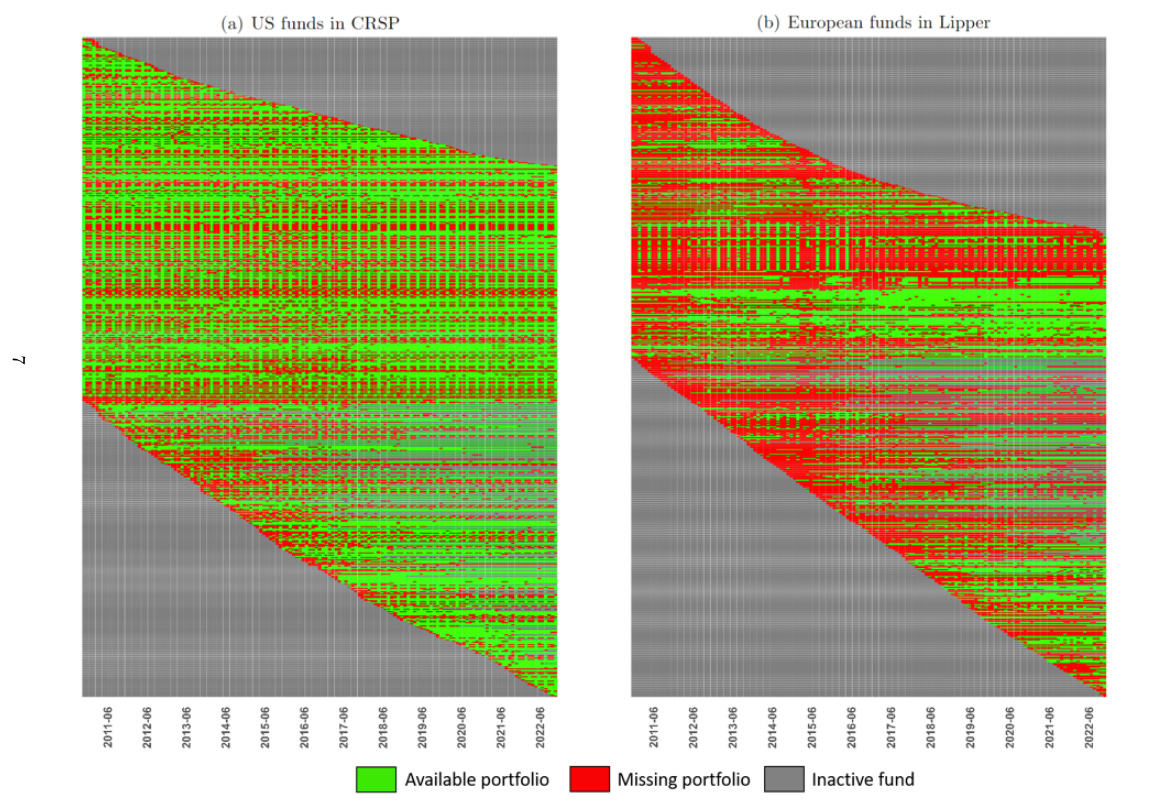

Missing Data Bias in Fund Portfolio Data: The paper warns of bias in commercial databases due to nonrandom portfolio reporting, which can lead to skewed conclusions in fund literature. (2024-07-17, shares: 2.0)

Market Liquidity Determinants: The study applies machine learning to identify factors affecting equity market l…