Quant Letter: May 2024, Week-2

Weekly (45th Edition)

SSRN

Recently Published

Quantitative

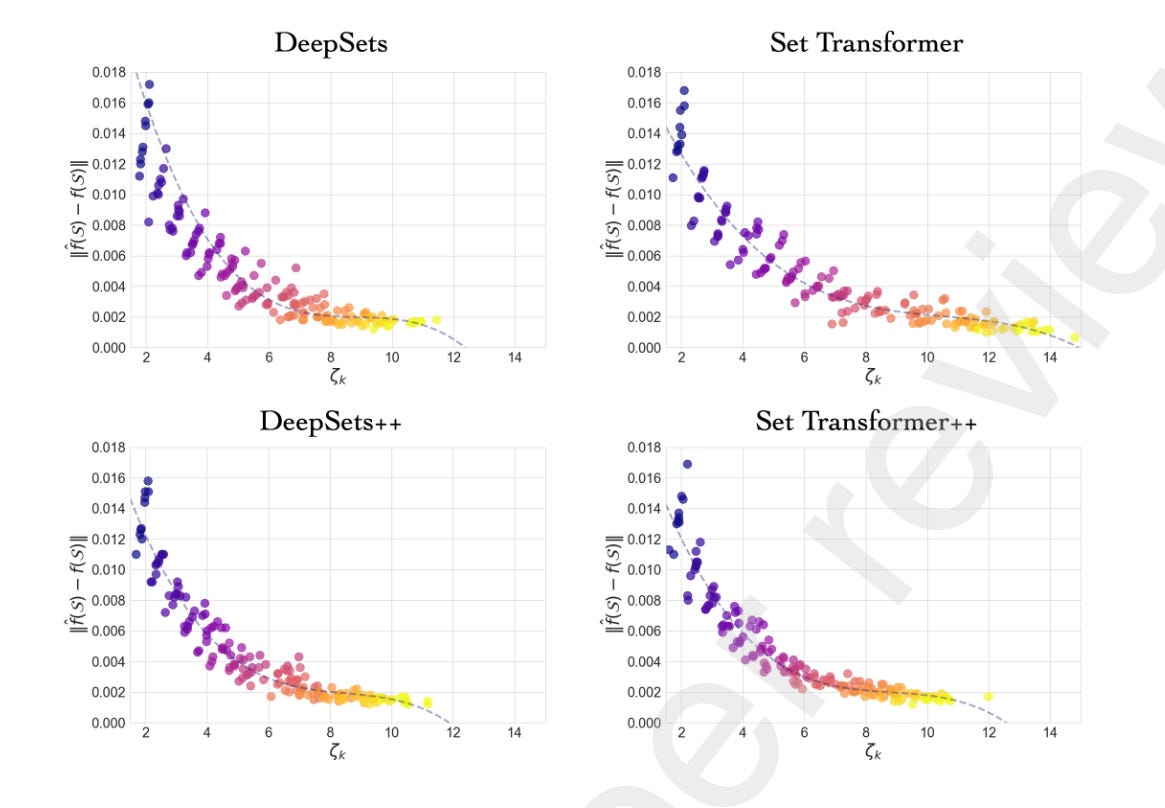

Permutation-Invariant NN Analysis: The study explores permutation-invariant neural networks, which can process various data formats and generate results unaffected by the input data's sequence. (2024-05-02, shares: 4.0)

Explainable Autoencoder Anomaly Detection: The suggested model uses an explainable variational autoenc…