Quant Letter: May 2025, Week-2

Weekly (91st Edition)

ArXiv

Finance

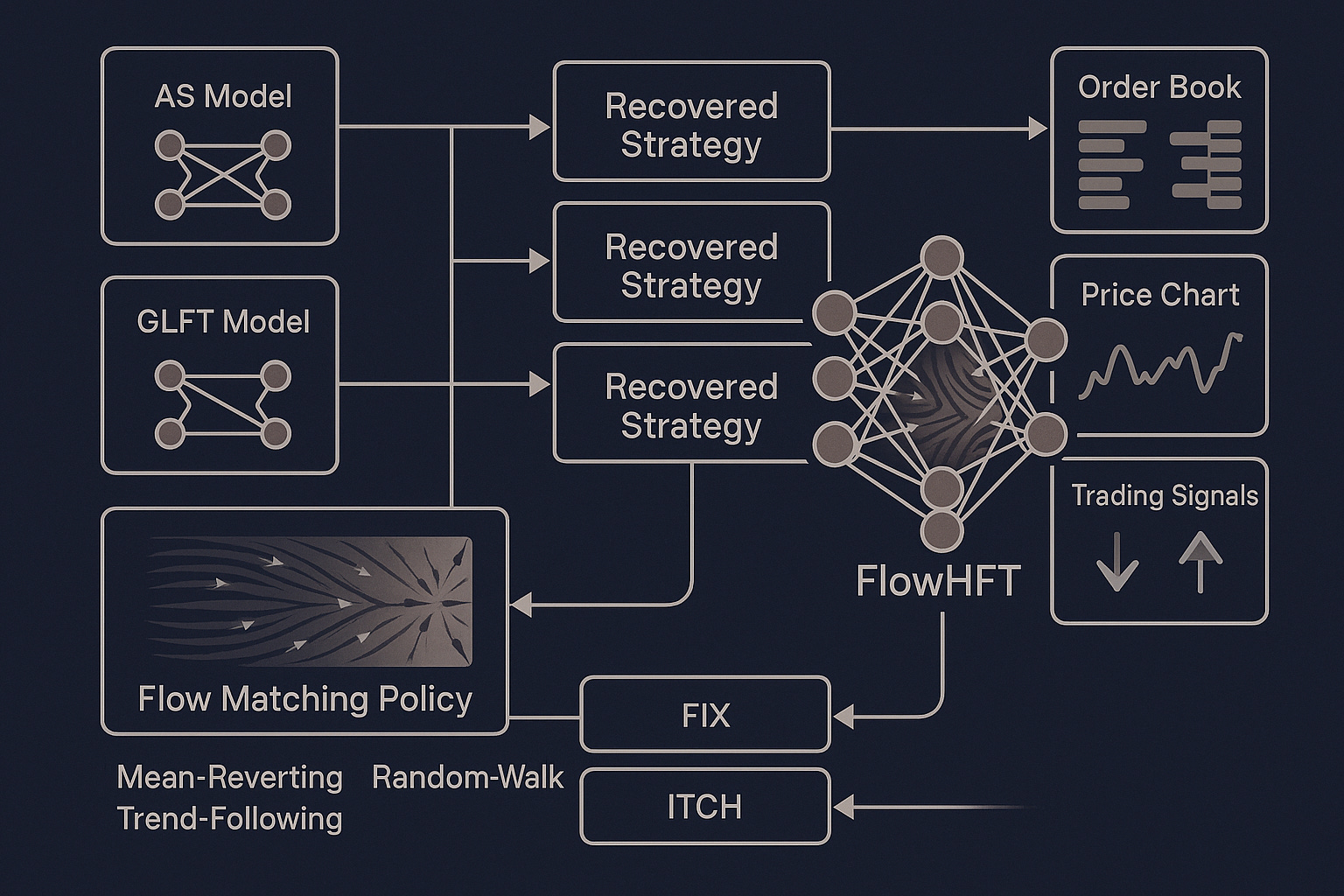

FlowHFT: High-Frequency Trading: FlowHFT, a new imitation learning framework, outperforms traditional high-frequency trading models by learning from multiple expert models. (2025-05-09, shares: 26)

Loss-Rebalancing in Blockchains: A study reveals that constant block intervals in blockchain settings provide the best protection against arbitrag…