Quant Letter: November 2023, Week 1

Research of the Week (23rd Edition)

ArXiv

Finance

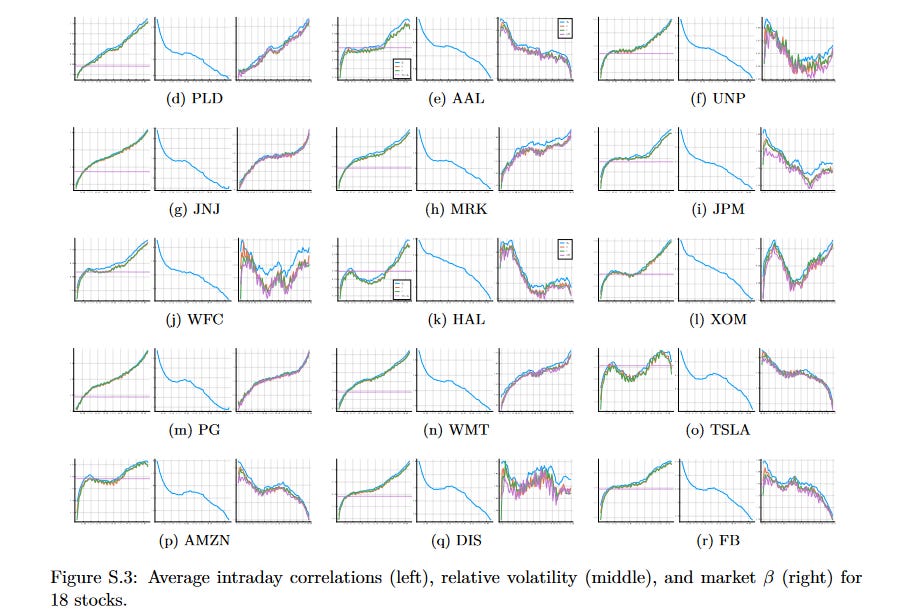

Estimating Realized Correlation in High-Frequency Financial Data: A new method for analyzing high-frequency financial data shows that intraday market changes are mainly driven by intraday correlation changes. (2023-10-30, shares: 5)

Agent-based Model for Deep Hedging: The Chiarella-Heston model, an advanced agent-based model, enhances deep he…