Quant Letter: November 2024, Week-3

Weekly (71st Edition)

ArXiv

Finance

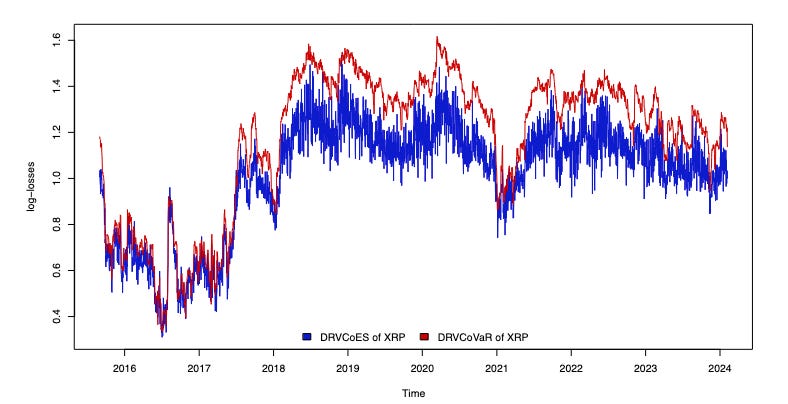

Vulnerability Conditional Risk Measures: The article introduces Vulnerability Conditional risk measures, a new systemic risk measure to assess tail risk during financial distress among market participants. (2024-11-14, shares: 2)

Asymptotics of Heavy-tailed Risks with Copulas: The research examines the tail asymptotics of the sum of two heavy…